Most recent results – The EPOC met on January 24, 2020 and reviewed the performance of the economy for the period ended November 2019.

EPOC reviewed the Quantitative Performance Targets and Priority Actions Matrix FY2019/20 – FY 2020/21 which formed the basis for the monitoring of the GOJ Economic Reform Programme (ERP) following the expiry of the IMF Stand-By Arrangement on November 10, 2019.

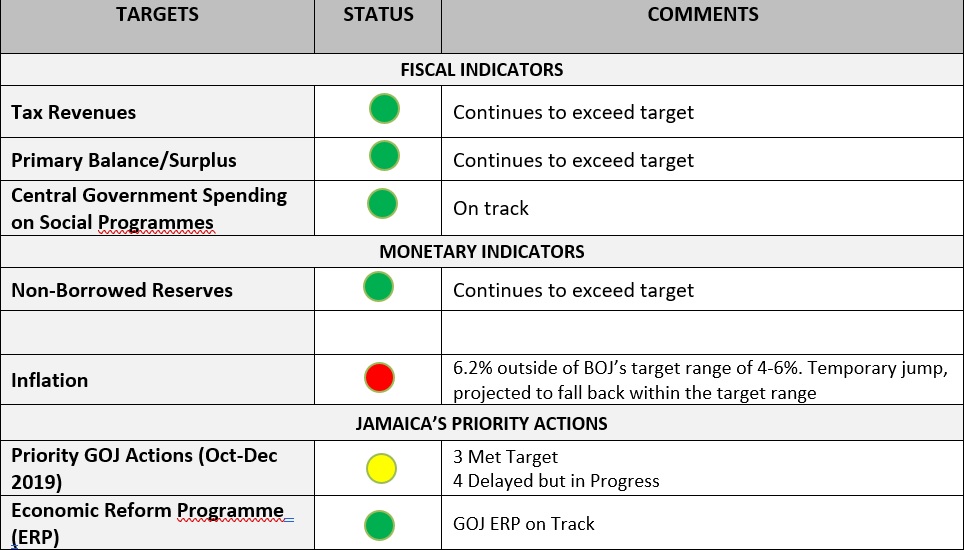

The GOJ ECONOMIC REFORM PROGRAMME IS ON TRACK

Based on the preliminary performance results to date through end-November 2019, the GOJ is on track to meet the Quantitative Performance Targets for the GOJ ERP for end-December 2019, with the exception of the inflation target.

Selected Quantitative Performance Targets and Policy Actions Status Updates

PROGRAMME REVIEW THROUGH NOVEMBER/DECEMEBER 2019

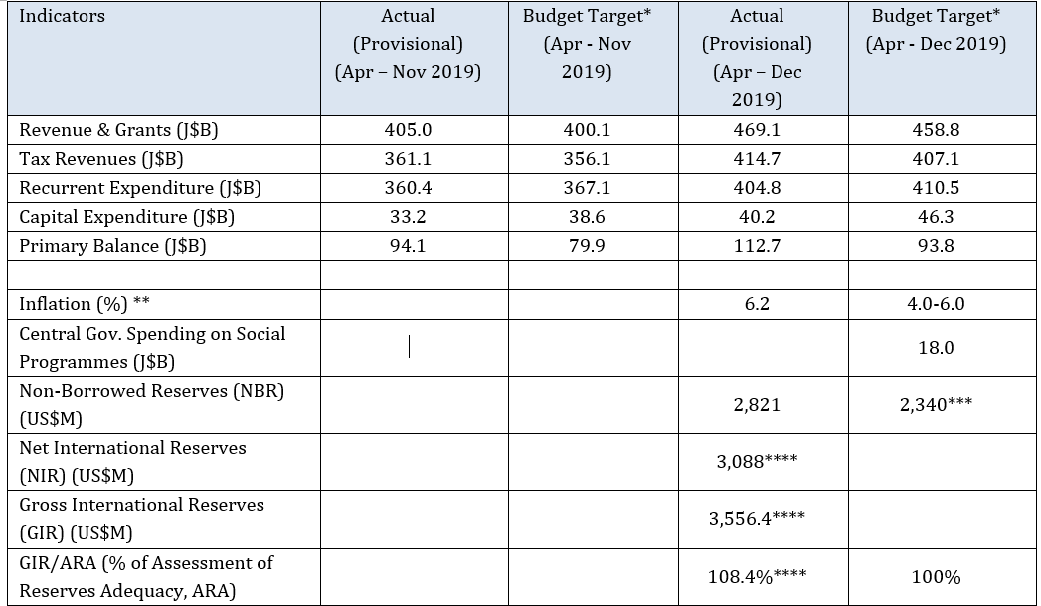

Selected GOJ Fiscal and Monetary Indicators

* 1st Supplementary Budget FY2019/20

**CPI point-to-point movement

***Adjusted target (as at January 8, 2020)

****As at January 22, 2020

Note: Apr-Dec 2019 fiscal data was available after EPOC met on January 24, 2020.

SELECTED FISCAL INDICATORS

Fiscal and Primary Surpluses exceed FY April – November 2019 Target

FISCAL BALANCE

For the fiscal year to date, April–November 2019, a fiscal surplus of $11.43B was recorded against a projected deficit of $5.52B for the same period. This positive performance was driven by higher than budgeted Revenue & Grants and the lower than budgeted Expenditure (excluding Amortization).

Revenues & Grants

Revenue & Grants of $405.0B, for the first eight months of the FY (April-November), outperformed the budgeted amount of $400.1B (+1.2%) mainly reflecting higher than projected Tax Revenues (+$5.0B).

Tax Revenues

Tax revenues of $361.1B exceeded the budget by $5.0B (+1.4%). The tax categories which contributed to higher than budgeted revenue were PAYE (+$2.7B), Special Consumption Tax (SCT) (+$2.6B), and Other Companies (+$1.7B). The main categories which underperformed were GCT (Local) (-$1.2B) and Tax on Interest (-$0.9B).

Expenditures

Recurrent & Capital Expenditure totaling $393.5B was below budget by 3.0% for the first eight months of the fiscal year. Of this amount, Recurrent Expenditure of $360.4B was $6.7B (-1.8%) below budget and Capital Expenditure of $33.2B was lower than budget by $5.4B (-14.1%). The lower than budgeted performance in Capital Expenditure was due to a delay in the execution of capital programmes, mainly the Southern Coastal Highway Improvement Project.

PRIMARY BALANCE EXCEEDS BUDGET TARGET BY $14.16 B

As a result of the higher than expected Revenue & Grants performance and the under-expenditure for the first eight months of the fiscal year, the Primary Balance of $94.1B exceeded the budget target of $79.9B for April-November 2019.

Second Supplementary Estimates tabled – January 21, 2020

Revenues & Grants for the fiscal year 2019/20 are currently projected to increase by $7.3B over the first supplementary estimates. Tax Revenues are projected to be the main contributor to the increase with additional inflows of $7.5B projected. Expenditures are projected to increase by approximately $8.0B which is broken out into recurrent programmes revised upwards by $7.2B and compensation of employees increased by $757.7M.

MONETARY TARGETS

International Reserves

As at end-December 2019, Net International Reserves stood at US$3.16B.

Non-Borrowed Reserves

The stock of Non-Borrowed Reserves of US$2.82B at end-December 2019 was US$480.5M above the adjusted targeted floor of US$2.34B.

Gross Reserves

As at January 22, 2019, gross reserves stood at US$3.56B, a decline of US$48.8M for the fiscal year to date (April-January 22). Gross reserves remain at 108.4% of the ARA metric.

Inflation

The annual point-to-point inflation rate as at December 2019 was 6.2 per cent stemming from faster increases in the prices of vegetables and starchy foods as well as energy-related prices. This was above BOJ’s target of 4.0 per cent to 6.0 per cent and was also higher than the 4.6 per cent recorded for November 2019 and 2.4 per cent in December 2018.

The higher than expected point-to-point inflation (6.2% as at December 2019) is expected to be temporary as downwards movements in agricultural prices are expected to dampen inflation over the next three to six months.

BOJ to report into Ministry of Finance on missed inflation target

As the inflation outturnwas outside of the target range, the Bank of Jamaica will have to provide a report to the Ministry of Finance for inflation being outside the target range and the corrective monetary policy actions, if any, that may be required.

Core Inflation

Core inflation, measured as the Consumer Price Index excluding the prices of Agricultural Commodities & Fuel remained at 2.9% for the month of December 2019 as it was in November 2019.

Foreign Exchange Market

The value of the Jamaican dollar at end-January, 2020 was J$141.22 to US$1.00, representing a depreciation of 6.5 per cent ($8.65) for the month. This was influenced by strong demand from end users, supported by significant net-buying in the Dealer segment following the holiday season.

On an annual basis, the Jamaican dollar at end-January, 2020 depreciated by 3.8 per cent ($5.12) similar to the depreciation of 3.8 per cent ($4.85) at the end of December 2019 and a depreciation of 6.3 per cent ($7.87) for the twelve months to January 22, 2019.

There were no B-FXITT sale or purchase operations during January. However, the BOJ on January 22, 2020, announced the introduction of a new instrument, the Foreign Exchange (FX) Swap Arrangement, which is available to foreign exchange authorized dealers (ADs). This instrument is intended to enhance the Bank’s management of the FX market, provide USD liquidity and price discovery. The Bank will sell US dollars to ADs, with a pre-defined limit, at a prevailing market rate, with an agreement to buy back the same amount of USD at a future date at an agreed forward rate.

BOJ holds policy rate at 0.5%

The BOJ maintained an accommodative policy stance as it held policy overnight interest rate unchanged at 0.50 per cent per annum, effective December 23, 2019.

Merchandise Trade

STATIN reported that Merchandise trade imports for January–September 2019 were valued at US$4,816.5M, an increase of 6.5 per cent relative to US$4,520.2M spent in the same period in 2018. Increased expenditure on food, Machinery and Transport Equipment and Mineral Fuels accounted for this outturn. Export earnings totaling US$1,268.7M were 9.1 per cent lower compared with the similar period in 2018.

Economic Growth

STATIN indicated that the Jamaican economy grew by 0.6 per cent for July–September 2019, representing the nineteen consecutive quarters of positive growth. This outturn was due, in part, to increases in Manufacturing (+4.9%), Finance & Insurance Services (+3.4%) and Hotels & Restaurants (2.5%). Higher growth was negatively impacted by a 17.6 per cent fall in the Mining & Quarrying industry which was largely due to the suspension of production in early September at the Jiuquan Iron and Steel Company (JISCO) Alpart refinery.

Labour Force Market

Jamaica’s unemployment rate at October 2019 was 7.2 per cent, which was lower than the 8.7 per cent at October 2018 and 7.8 per cent at July 2019. The fall in the unemployment rate reflected a decline of 19,000 in the number of unemployed persons which was partially offset by growth of 10,200 persons in the labour force.

The employed labour force for October 2019 was 1,248,400, an increase of 29,200 relative to October 2018. The number of employed males increased by 10,600 to 682,800 and employed females by 18,600 to 565,600.

JAMAICA’S PRIORITY REFORM ACTIONS

The completion of the sixth review under the SBA included the approval of Priority Actions Matrix for FY2019/20-FY2020/21, which formed part of the basis for the monitoring of the GOJ Economic Reform Programme (ERP) following the expiry of the SBA.

The GOJ has met three (3) of the seven (7) reform areas under the Priority Actions for the monitoring of the GOJ ERP for the period October–December 2019. The remaining four have been delayed but are in progress.

EPOC’s OUTLOOK

Economic Growth

The World Economic Outlook (WEO) is projecting global growth to rise from an estimated 2.9% in 2019 to 3.3% in 2020 while growth in the Latin American and Caribbean region is expected to rebound to 1.6% in 2020. The Planning Institute of Jamaica projects Jamaica’s real GDP growth for the fiscal year 2019/20 to fall within the range of 0.0%–1.0%.

EPOC concurs with the view of the PIOJ that growth will be low for the remainder of the fiscal year 2019/20. However, EPOC expects that going forward through 2020-2022, growth should begin to get back to the 2% growth levels, as the impact of the fallout from mining is behind us.

Monetary Performance

While point-to-point inflation of 6.2% as at December 2019 was outside of the BOJ target range, it is expected to be temporary hence the BOJ will maintain its accommodative monetary policy stance. BOJ expects inflation for the next 12 months ending November 2020 to be much lower than the rate that obtained in December 2019. The results of the Bank’s Inflation Expectations Survey suggests that market participants expect inflation to be 5.0%, owing largely to inflationary trends and exchange rate changes.

Credit Growth

This accommodative stance continues to spur Credit growth from the Deposit taking Institutions as credit to businesses and households increased by 15.5% between September 2018 to September 2019.

International Reserves

Jamaica’s net international, non-borrowed and gross international reserves continue to exceed programme targets and exceed the international adequacy benchmark.

Fiscal Performance

The fiscal performance continues to be strong as tax revenues continue to outperform budget and the first supplementary budget targets which led to a second supplementary budget being tabled in parliament for Fiscal year 2019/20.

Foreign Exchange Market

As there continues to be market apprehension and a heightened uncertainty around the volatility of the exchange rate, the BOJ continues its ongoing dialogue with the market in an effort to reduce volatility and smooth out demand and supply imbalances. The BOJ recently introduced a FX Swap Arrangement and are encouraging authorized dealers and cambios to further deepen the market through the introduction of forward contracts while looking to the implementation of the electronic trading platform in early 2020. These improvements will provide greater transparency and price discovery for market players.

EPOC acknowledges BOJ’s efforts to deepen the FX market and notes the ongoing consultations with the Jamaica Bankers Association and other key stakeholders in the market.

EPOC is hopeful that as the reforms in the FX market take hold, volatility levels and the swings in the currency could be reduced. However, Jamaica is only a very small player in the global FX market and will always be exposed to and not insulated from volatility and movements in the international FX market.

EPOC Post IMF

Following the completion of the three-year Precautionary Stand-By Arrangement (PSBA) with the IMF as at November 2019, EPOC continues to serve under a new Memorandum of Understanding. Under this agreement, EPOC’s extended period of service will be aligned with the establishment of the Fiscal Council and completion of activities related to the Central Bank achieving Independent status.

This information is provided to you monthly by the non-public sector members of EPOC